BIZCHINA> Review & Analysis

|

BIZCHINA> Review & Analysis

|

|

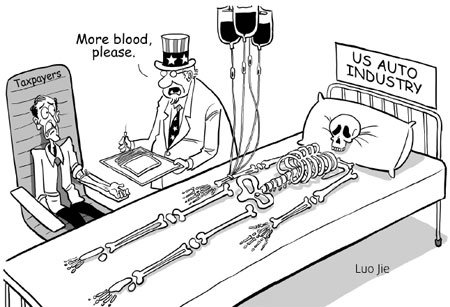

GM plan could drive bond market crazy

By James K. Glassman (China Daily)

Updated: 2009-06-03 14:03

What's my interest in this? I head a nonprofit group that encourages developing nations to adopt policies that will lead to prosperity - starting with transparency and the rule of law - and hold up America as a model. Yet in its high-handed dealings with Chrysler and GM, the Obama administration reminds me of an irresponsible third-world regime, skirting the law and handing economic prizes to political cronies. GM has filed for bankruptcy, and under its complicated plan, bondholders - ranging from large institutions to low-income retirees - would receive just 10 percent of the reorganized company, plus warrants that would enable them to get 15 percent more should the company's value reach certain levels, in return for their $27 billion in loans. The government, which could end up putting $70 billion into GM, would initially get 72.5 percent of the company. In return for money GM owes its health trust, the auto workers' union would get 17.5 percent of its stock, warrants to raise that share to 20 percent, along with a $2.5 billion cash payout over eight years and $6.5 billion in preferred stock paying a 9 percent dividend. I agree with bondholders who feel the union is getting at least four times as much of GM in return for claims that are, at best, equal to those of the creditors. The administration's actions in trying to force the deals may damage the credit markets for years to come. The treatment of the bondholders is a warning to investors that the federal government won't hesitate to push them aside in a crisis.

Perhaps it's no coincidence that in the wake of the Chrysler deal we have seen a decline in prices for long-term Treasury bonds and a sinking dollar. The hardball tactics, furthermore, are unlikely to save GM. In a normal bankruptcy, the company's assets pass from weak hands to strong. In 2008, a terrible year for the auto industry, GM sold 8.4 million vehicles worldwide, collecting revenues of $148 billion that placed it third among non-energy companies on the Fortune 500. GM is a global business, with two-thirds of its revenues coming from outside the United States. While sales last year dropped 21 percent in North America, they rose 30 percent in Russia, 10 percent in Brazil and 9 percent in India. In 2008, GM sold more than one million vehicles in China, up 6 percent over 2007. The company's problem, of course, is that its expenses exceed its revenues. But in strong hands, GM could be a going concern. Unfortunately, the new owners, with about nine-tenths of the shares, will be the government and the UAW. These are the same hands that shaped much of GM's trouble in the first place. With substantial union co-ownership, labor costs won't be contained; and with the government as the boss, politics may trump markets in decisions on such matters as where to put plants and whether to build big cars or small ones. The deal would also put GM's competitors at a serious disadvantage in the short run. Ford, which has been building better cars lately, prudently raised cash against a decline in demand, playing the ant to GM's grasshopper. Now, Ford will face a GM buoyed by taxpayer dollars both for manufacturing and for cheap consumer and dealer financing. The same holds true for the manufacturers that hold the key to future auto-making jobs: well-managed, foreign-based companies like Toyota and Honda, which, according to the automotive analysts at CSM Worldwide, will build more cars in the United States next year than GM, Chrysler and Ford combined. What lesson does federal favoritism toward Chrysler and GM teach other businesses that play by the rules? How will our trade negotiators keep a straight face when complaining about subsidies to Airbus or Chinese steel makers? The government should have stepped aside earlier and allowed a normal bankruptcy that would have treated the union and the debt-holders fairly. The author was under secretary of state for public diplomacy and public affairs in the George W. Bush administration. He is now the president of World Growth, a nonprofit economic-development group. The New York Times Syndicate (For more biz stories, please visit Industries)

|

|||||

磴口县| 谢通门县| 临漳县| 蒲江县| 沙河市| 朔州市| 津市市| 榆中县| 巴林左旗| 泊头市| 浦东新区| 常德市| 阜阳市| 老河口市| 加查县| 天气| 连云港市| 漳平市| 吴川市| 兴山县| 荔浦县| 百色市| 金乡县| 娄底市| 张家界市| 龙口市| 灌云县| 启东市| 扎鲁特旗| 西和县| 嵩明县| 宜州市| 阿鲁科尔沁旗| 乡城县| 张家界市| 临海市| 乌兰浩特市| 治县。| 新竹市| 麻江县| 咸宁市|