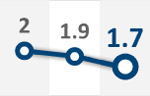

China's economy is slowing. Since 2002 China's annual real GDP growth has always been above 9 percent year-on-year; this may not be the case in 2012. Real GDP growth slowed to 8.1 percent year-on-year in the first quarter of this year; down from 8.9 percent in the fourth quarter of 2011, and recent data in April suggest that a strong rebound is not on the cards.

The slowdown can be attributed to the impact of slowing external demand on China's export sector as well as the deliberate policy to discourage unproductive investment. This is not necessarily a cause for concern. One should not see growth of less than 9 percent as a sign of China losing its competitiveness. China's current focus on the sustainability of growth is appropriate. What is important is that growth remains sufficient to absorb new job seekers and continues to deliver the income growth that improves the livelihood of the majority of the population. Judging from the experience of other countries, achieving strong economic growth but having the wealth concentrated among a minority of the population will create problems later on.

Most economists, including Deutsche Bank's, continue to expect China's real GDP growth to stay above 8 percent year-on-year in 2012 and 2013. This is not a disaster for China, especially considering that demand from key trading partners such as the United States and the European Union is unlikely to grow as strongly as it did in the past decade. As for domestic demand in China itself, there is indeed untapped potential. However, it is correct to tread cautiously in order to avoid over-stimulating to the extent of creating overheating or new asset bubbles, which would lead to a hard landing.

The current situation in China can be described as a soft landing. Quarterly real GDP growth slowed from the double-digit rates of 2006-08 and during the late-2009, early-2010 period to the current 8-9 percent year-on-year. One should also not forget that years of strong growth and demand have also led to higher inflation, which averaged 1.5 percent year-on-year during 2002-06 and climbed to 3.7 percent year-on-year during 2007-11. This highlights the fact that managing inflation and inflation expectations should also receive high priority in addition to ensuring sufficient growth.

We should also be mindful of the difference between the situation now and the situation in 2008-09. In late 2008, China's growth did not slow; it plummeted. Real GDP growth dropped from 9 percent year-on-year in the third quarter of 2008 to 6.8 percent in the fourth quarter of 2008. The current situation is rather different, since the slowdown has been gradual and orderly. Real GDP slowed steadily from 9.8 percent year-on-year in the fourth quarter of 2010 to 8.1 percent in the first quarter of 2012.

Even the property market correction has so far been playing out orderly in key cities. If a fiscal stimulus is needed now, it will be different from 2008-09 by virtue of the different circumstances. Furthermore, critics observe that local Chinese banks stepped up lending, a form of "off-budget stimulus" during 2009, which led to rising concerns over the viability of bank debts owed by local government financing vehicles, a potential source of contingent liabilities for the central government.

Since these worries still exist, the central government is understandably less inclined to introduce a similar kind of stimulus package. Last but not least, the authorities will be ultra cautious to avoid creating another housing bubble. This explains their reluctance to unwind some of the curbs on real estate.

Having raised the aforementioned points, we are not ruling out the possibility of some form of fiscal stimulus should growth slow down further to the point that job security for ordinary people is threatened and social stability is jeopardised. In a scenario where global risks heighten and external demand plunges further, China's growth will be adversely affected.

Still, the point remains that the central government is likely to tread more cautiously than in 2008-09. The stimulus package will possibly be more targeted at preserving jobs in order to support income and private spending. For example, firms may be given incentives or even financial assistance to retain rather than fire workers if demand is expected to rebound in the foreseeable future. Some of the long-term infrastructure projects could be moved forward.

In addition, it has recently been reported that the authorities will focus on encouraging private investment in areas such as railways, infrastructure, healthcare and education. These targeted investments, aimed at expanding the needed capacity in physical infrastructure and social services, will complement China's long-term objectives to support domestic demand.

In short, while fiscal stimulus may not appear to be urgently needed now, it may be needed if external risks continue to mount. What is important is the authorities remain alert and measure their response, rather than adopting a "kick-the-can-down-the-road" approach in their handling of the current downturn. This bodes well for the country's long-term prospects.

The author is a senior economist at Deutsche Bank.

Copyright 1995 - 2010 . All rights reserved. The content (including but not limited to text, photo, multimedia information, etc) published in this site belongs to China Daily Information Co (CDIC). Without written authorization from CDIC, such content shall not be republished or used in any form. Note: Browsers with 1024*768 or higher resolution are suggested for this site.

License for publishing multimedia online 0108263 Registration Number: 20100000002731 ![]()